One of the biggest financial uncertainties in 2025 is the fate of the Tax Cuts and Jobs Act (TCJA). Many of its provisions are set to expire at the end of the year, which could lead to significant tax changes affecting income brackets, business deductions, and estate planning. While the final outcome remains unknown, taking steps now can help you prepare for different scenarios.

Key Financial Planning Changes for 2025

Here’s a breakdown of what’s changing and how proactive planning can help you stay ahead.

1. IRS Tax Bracket Adjustments & Standard Deduction Increases

Each year, the IRS adjusts tax brackets to account for inflation. In 2025, income thresholds are increasing by about 2.8%—a smaller adjustment than the 5.4% increase in 2024 and 7% in 2023. While this helps prevent inflation from pushing you into a higher tax bracket unnecessarily, reviewing your income timing strategies now can help optimize your tax bill.

Standard Deduction Increases:

- Single filers: $15,000 (up $400 from 2024)

- Married filing jointly: $30,000 (up $800 from 2024)

- Head of household: $22,500 (up $600 from 2024)

2. Estate & Gift Tax Exemptions Are Rising

If estate planning is part of your financial strategy, take note of these increases:

- Lifetime Gift Tax Exemption: $13,990,000 per person (an increase of $380,000 from 2024)

- Annual Gift Tax Exclusion: $19,000 per recipient (an increase of $1,000 from 2024)

While this gives you more flexibility to transfer wealth tax-efficiently, keep in mind that unless Congress acts, the exemption could drop to around $7 million per person in 2026. If you have a taxable estate, reviewing how these changes align with your long-term goals, liquidity needs, and family priorities can help ensure your planning remains effective beyond just tax considerations.

3. What’s at Stake if the Tax Cuts and Jobs Act Expires?

Without Congressional action, several key tax benefits could disappear, including:

- Higher individual tax rates (Top bracket increasing from 37% to 39.6%)

- Estate tax exemption cuts (Dropping from $13.99 million to around $7 million per person, depending on inflation)

- Elimination of the 20% Qualified Business Income (QBI) Deduction for pass-through businesses

- Further phase-out of bonus depreciation for businesses

- Continuation of the $10,000 cap on State and Local Tax (SALT) deductions

With tax policy decisions on the horizon, acting now to review your income strategy, wealth transfer plans, and business deductions could help you maximize current tax rules before they potentially change.

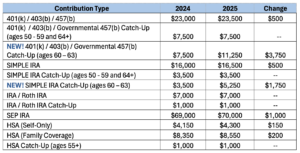

4. Retirement Contribution Limits Are Increasing

Maximizing tax-advantaged savings is more beneficial than ever with these higher contribution limits:

5. New! Super Catch-Up Retirement Contributions for Ages 60-63

For those between 60-63, the catch-up contribution limit for 401(k) and similar plans jumps to $11,250, a $3,750 increase. Similarly, the SIMPLE IRA catch-up rises to $5,250, up $1,750. Planning ahead by adjusting your payroll elections now can ensure you maximize these new savings opportunities.

The Power of Proactive Financial Planning

With tax laws in flux and retirement contribution limits on the rise, making proactive financial decisions now could be more important than ever. Some changes—like higher contribution limits—are already in place, while others, such as TCJA provisions, remain uncertain.

The best strategy? Take control of your financial future now.

- Maximize tax-advantaged savings before contribution deadlines.

- Review estate planning strategies before potential exemption cuts in 2026.

- Reassess business deductions to leverage current tax rules before possible changes.

While no one knows exactly how tax policy will unfold, taking action today puts you in the best position—giving you more options, greater flexibility, and fewer surprises in the years ahead.

If you’re a current client and have questions about how these changes impact your financial plan, don’t hesitate to reach out. If you’re not yet a client but want guidance on how to proactively plan for 2025 and beyond, we’re here to help—schedule a consultation to get started.

This material is for educational purposes only and is not intended to provide specific advice or recommendations for any individual and does not take into consideration your specific situation. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Be sure to consult with a qualified financial advisor, legal, and/or tax professional before implementing any strategy discussed here.

This material is for educational purposes only and is not intended to provide specific advice or recommendations for any individual and does not take into consideration your specific situation. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Be sure to consult with a qualified financial advisor, legal, and/or tax professional before implementing any strategy discussed here.