Wealthy investors often operate in a more complex environment than the average market participant. Elevated valuations, rapid technological shifts, evolving monetary policy, and global uncertainty create both opportunity and risk. For ultra- and high-net-worth families, the real challenge is avoiding the subtle mistakes that can undermine long-term durability.

Over decades of advising affluent families, we’ve seen certain patterns repeat. Strong markets encourage overconfidence. Volatility exposes weak assumptions. Tax inefficiency compounds quietly. And portfolios that once felt intentional can drift without coordination.

What Are the Most Common Mistakes Wealthy Investors Make?

Wealthy investors often struggle with unrealistic return expectations, lifestyle inflation during bull markets, tax inefficiency, overconcentration, and a lack of an integrated strategy.

Below are eight common investment mistakes along with practical ways to stay disciplined, diversified, and prepared for a range of outcomes.

1. Expecting Market Returns to Be “Average”

Why Average Returns Are Misleading

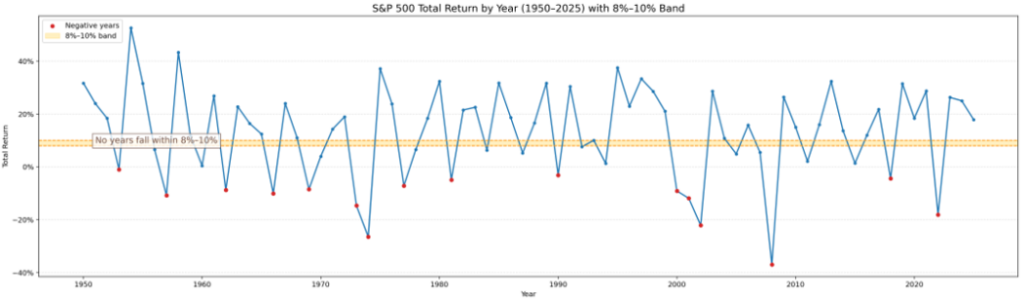

Most investors think of the S&P 500 averaging roughly 8–10% annually over long stretches. Reality shows the index rarely lands in that range in any given year. As illustrated below, returns for the index didn’t fall into that range even once over the past 75 years. Typically returns are meaningfully higher or lower, sometimes dramatically.

Distribution of S&P 500 Annual Returns Over 75 Years

Source: Slickcharts

Investor takeaway: Don’t anchor on averages. Have a mindset that stock returns vary significantly, then think of that volatility as the “toll” for higher long-term performance.

2. Spending Like the Bull Market Will Last Forever

Why Every Wealthy Family Needs a Plan B

Strong markets create a powerful illusion: “My portfolio is growing… I must be fine.”

But rising asset values can quietly mask two risks — expanding lifestyle costs and creeping leverage. When markets are strong, those decisions rarely feel dangerous. When markets decline, they become very visible.

Even very wealthy families may need — or simply prefer — to adjust spending during severe downturns. The difference between confidence and stress is rarely net worth. It’s whether those adjustments were thoughtfully considered in advance.

A well-designed Plan B provides optionality.

It means knowing:

- Which expenses are essential

- Which are lifestyle choices

- Which can be deferred without changing your long-term trajectory

Your Plan B might include:

- Deferring major purchases or capital-intensive projects

- Temporarily scaling back luxury travel or discretionary experiences

- Reducing carrying costs by selling one of several homes

- Modifying or pausing financial support for adult children

When flexibility is intentional, adjustments become part of a strategic plan.

Investor takeaway: If your lifestyle depends on strong markets, your financial plan lacks durability. Confidence comes from knowing you could adapt rather than assuming you’ll never need to.

3. Spending Too Little and Deferring Life

On the flip side, one of the most common, but least discussed, mistakes among wealthy investors is optimizing portfolios while deferring life. As Bill Perkins notes in Die With Zero, “your life energy is limited.” For some, the real risk isn’t outliving your assets; it’s postponing meaningful experiences until health, time or family dynamics make them impossible, leaving behind a strong balance sheet but an under-lived life. As my business partner, Joe Mackey, says, “don’t just leave your legacy, live your legacy.”

Fear of running out keeps some wealthy investors from enjoying experiences for themselves and their families.

Three steps can help you plan with confidence:

- Estimate your likely annual withdrawals. This seems obvious, but you’d be surprised how often very wealthy individuals fail to create even a high-level budget. As a result, they never become truly comfortable with their spending because they haven’t done the math.

- Ensure your asset allocation aligns with the required return. Is your investment mix assuming too much risk, or not enough to meet the return target for your needs?

- Run Monte Carlo simulations to assess long-term sustainability. What is the likelihood, statistically, that your money will last?

Investor takeaway: If you’re already working with us, you’ve likely walked through these steps in recent reviews. It’s always helpful to revisit the numbers and ensure they still reflect reality.

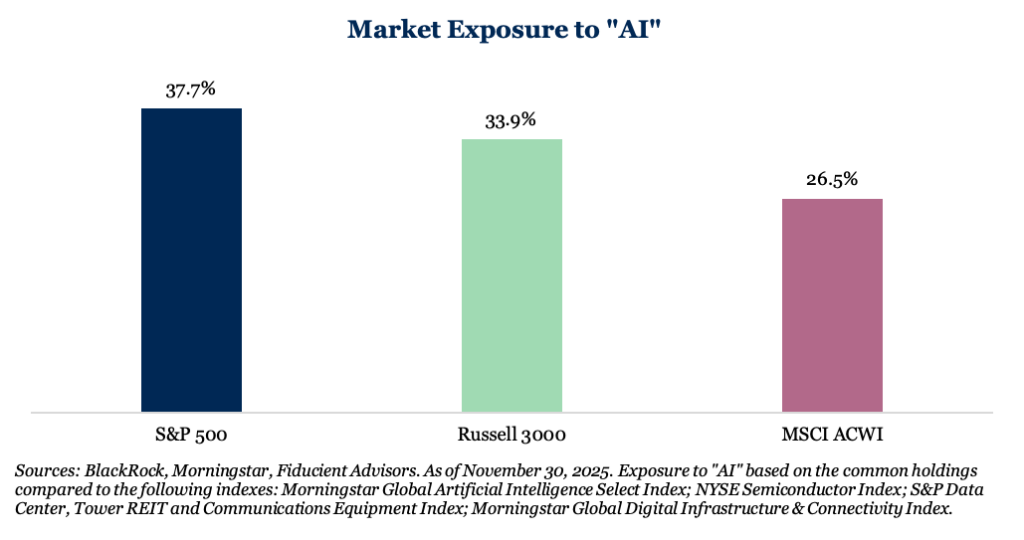

4. Underestimating Exposure to AI and Market Concentration

Some investors tell us, “I’m not chasing AI stocks.” But if you own broad index funds, you own AI through hyperscalers like Microsoft, Alphabet, Amazon and through companies powering AI infrastructure such as semiconductors, data centers and energy providers.

AI has been a primary driver of recent market returns. But valuations are stretched, and history shows that disruptive technologies produce big winners and many losers.

Investor takeaway: Understand your exposure to AI. Being overexposed introduces risk; having zero exposure misses opportunity.

5. Failing to Diversify Broadly

With lofty valuations, rising deficits and growing geopolitical uncertainty, diversification matters now more than ever.

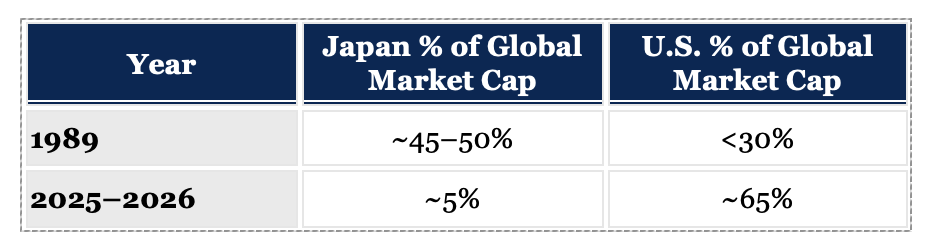

History provides a powerful reminder. In 1989, Japanese equities represented roughly 50% of global stock market capitalization, and I think you’d be surprised to learn (or remember) that eight of the world’s ten largest companies were Japanese! The momentum appeared unstoppable. What followed were decades of stagnation. And today? Japan comprises only about 5% of global equity market capitalization.

The Need to Diversify: Shifting Global Landscapes

Sources: Credit Suisse Global Investment Returns, MSCI ACWI / ACWI IMI, Visual Capitalist, LPL Research

With the U.S. today accounting for nearly two-thirds of global market capitalization, the lesson is not that the U.S. will necessarily repeat Japan’s experience. Rather, it is that market leadership changes, often in ways few investors anticipate. Periods of extreme dominance, no matter how compelling the narrative, have historically proven temporary.

Investor takeaway: Concentration builds wealth; diversification preserves it. Business owners and executives with concentrated stock positions understand this instinctively. Thoughtful diversification can include not only diversifying equity holdings but adding bonds, real assets, private markets and more.

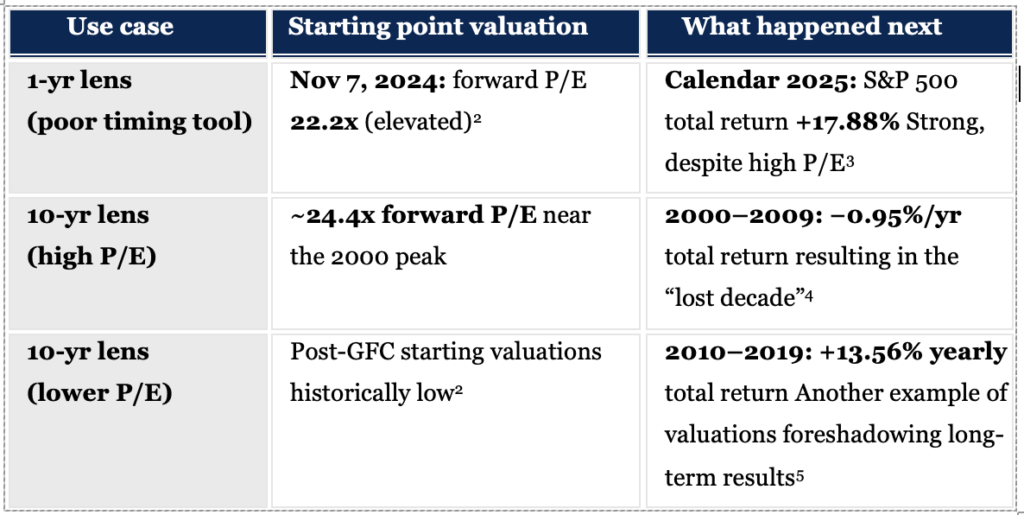

6. Assuming High Valuations Mean a Crash Is Imminent

Do High Valuations Predict a Market Crash?

Yes, valuations are elevated with the S&P 500 trading at a forward P/E of approximately 22 compared to the 25-year average of 16.7.[1]

But here’s an important insight: Valuations are poor predictors of performance over the short-term.

High valuations can stay high or move higher. Low valuations can remain depressed for extended periods. The following illustrates why valuations matter far more over longer horizons than over short ones.

Sources FactSet, dimensional.com, sparkwealthadvisors.com, ishares.com, slickcharts.com

Investor takeaway: Use valuations to set reasonable long-term expectations, not to time markets.

7. Failing to Control What You Can: Taxes

Why Tax Efficiency Compounds Over Time

Markets are unpredictable. Tax drag is not. And unlike markets, it compounds quietly and predictably.

For high-net-worth families, taxes are often the single largest “expense” on investment returns yet they’re frequently treated as an afterthought. The difference between pre-tax performance and after-tax wealth can compound meaningfully over time.

Unnecessary realized gains, poor asset location, short-term trading, and missed loss harvesting opportunities can widen the gap between what markets deliver and what investors actually keep. To be tax efficient, you need to be intentional. That includes:

- Thoughtful asset location — placing tax-inefficient assets in tax-advantaged accounts

- Capital gain budgeting — managing when and how gains are realized

- Systematic tax-loss harvesting — turning volatility into opportunity

- Direct indexing strategies — creating personalized loss harvesting at the individual security level

- Municipal bonds where appropriate — generating federal tax-free income for high earners

These decisions may seem incremental in isolation. Over years and decades, they compound into meaningful after-tax advantages. Tax efficiency is not a year-end task. It’s an ongoing discipline woven into portfolio construction and monitoring.

Investor takeaway: It’s not what you earn — it’s what you keep. A durable strategy is built with after-tax outcomes in mind.

8. Managing Your Wealth Without an Integrated Strategy

The final (and often most costly) mistake is letting wealth drift without intentional direction. Business ventures, careers, family, health and more all compete for your attention. You make decisions incrementally, quietly add positions to portfolios, and leave assumptions unexamined. What began as a thoughtful approach can slowly turn into a set of disconnected choices.

But strong outcomes rarely happen by accident. They come from clarity of priorities, disciplined decision-making and ongoing integration across goals, spending, investments, risk, liquidity and tax strategy. Life does get busy. This is precisely why it’s essential to assemble the right team of advisors who understand your objectives, challenge your assumptions and keep your plan on course when markets or life circumstances become uncomfortable or complex.

Investor takeaway: Without a clear strategy and someone accountable for coordinating it, even smart decisions can lead you off course.

Final Thoughts: Preparing for a Range of Outcomes

Innovation, resilient earnings, and supportive policy trends often fuel markets. At the same time, elevated valuations and ongoing uncertainty remind us that risk never disappears. Progress and volatility can coexist.

The objective is not to predict what happens next. It is to prepare for a range of outcomes. Be intentional in how you deploy capital across investments, spending, philanthropy and legacy. Durability rarely happens by accident. And as always, if you or someone you care about would benefit from thoughtful guidance, please reach out to me or any of us at MKD Wealth.

Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on MKD Wealth research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss. Benchmark and index performance results do not represent any managed portfolio returns. An investor cannot invest directly in a presented index, as an investment vehicle replicating an index would be required. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from index performance shown. The following indexes are referenced in the content above:

- The S&P 500 Index is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

- Russell 3000 Index is a market-cap-weighted index which consists of roughly 3,000 of the largest companies in the U.S. as determined by market capitalization. It represents nearly 98% of the investable U.S. equity market.

- MSCI ACWI (All Country World Index) captures large and mid cap representation across Developed Markets (DM) and Emerging Markets (EM) countries. The index covers approximately 85% of the global investable equity opportunity set.

[1] Jan. 8, 2026: Trendonify and FactSet

[2] ishares.com

[3] dimensional.com

[4] sparkwealthadvisors.com

[5] slickcharts.com

Wealthy investors often operate in a more complex environment than the average market participant. Elevated valuations, rapid technological shifts, evolving monetary policy, and global uncertainty create both opportunity and risk. For ultra- and high-net-worth families, the real challenge is avoiding the subtle mistakes that can undermine long-term durability.

Over decades of advising affluent families, we’ve seen certain patterns repeat. Strong markets encourage overconfidence. Volatility exposes weak assumptions. Tax inefficiency compounds quietly. And portfolios that once felt intentional can drift without coordination.

What Are the Most Common Mistakes Wealthy Investors Make?

Wealthy investors often struggle with unrealistic return expectations, lifestyle inflation during bull markets, tax inefficiency, overconcentration, and a lack of an integrated strategy.

Below are eight common investment mistakes along with practical ways to stay disciplined, diversified, and prepared for a range of outcomes.

1. Expecting Market Returns to Be “Average”

Why Average Returns Are Misleading

Most investors think of the S&P 500 averaging roughly 8–10% annually over long stretches. Reality shows the index rarely lands in that range in any given year. As illustrated below, returns for the index didn’t fall into that range even once over the past 75 years. Typically returns are meaningfully higher or lower, sometimes dramatically.

Distribution of S&P 500 Annual Returns Over 75 Years

Source: Slickcharts

Investor takeaway: Don’t anchor on averages. Have a mindset that stock returns vary significantly, then think of that volatility as the “toll” for higher long-term performance.

2. Spending Like the Bull Market Will Last Forever

Why Every Wealthy Family Needs a Plan B

Strong markets create a powerful illusion: “My portfolio is growing… I must be fine.”

But rising asset values can quietly mask two risks — expanding lifestyle costs and creeping leverage. When markets are strong, those decisions rarely feel dangerous. When markets decline, they become very visible.

Even very wealthy families may need — or simply prefer — to adjust spending during severe downturns. The difference between confidence and stress is rarely net worth. It’s whether those adjustments were thoughtfully considered in advance.

A well-designed Plan B provides optionality.

It means knowing:

Your Plan B might include:

When flexibility is intentional, adjustments become part of a strategic plan.

Investor takeaway: If your lifestyle depends on strong markets, your financial plan lacks durability. Confidence comes from knowing you could adapt rather than assuming you’ll never need to.

3. Spending Too Little and Deferring Life

On the flip side, one of the most common, but least discussed, mistakes among wealthy investors is optimizing portfolios while deferring life. As Bill Perkins notes in Die With Zero, “your life energy is limited.” For some, the real risk isn’t outliving your assets; it’s postponing meaningful experiences until health, time or family dynamics make them impossible, leaving behind a strong balance sheet but an under-lived life. As my business partner, Joe Mackey, says, “don’t just leave your legacy, live your legacy.”

Fear of running out keeps some wealthy investors from enjoying experiences for themselves and their families.

Three steps can help you plan with confidence:

Investor takeaway: If you’re already working with us, you’ve likely walked through these steps in recent reviews. It’s always helpful to revisit the numbers and ensure they still reflect reality.

4. Underestimating Exposure to AI and Market Concentration

Some investors tell us, “I’m not chasing AI stocks.” But if you own broad index funds, you own AI through hyperscalers like Microsoft, Alphabet, Amazon and through companies powering AI infrastructure such as semiconductors, data centers and energy providers.

AI has been a primary driver of recent market returns. But valuations are stretched, and history shows that disruptive technologies produce big winners and many losers.

Investor takeaway: Understand your exposure to AI. Being overexposed introduces risk; having zero exposure misses opportunity.

5. Failing to Diversify Broadly

With lofty valuations, rising deficits and growing geopolitical uncertainty, diversification matters now more than ever.

History provides a powerful reminder. In 1989, Japanese equities represented roughly 50% of global stock market capitalization, and I think you’d be surprised to learn (or remember) that eight of the world’s ten largest companies were Japanese! The momentum appeared unstoppable. What followed were decades of stagnation. And today? Japan comprises only about 5% of global equity market capitalization.

The Need to Diversify: Shifting Global Landscapes

Sources: Credit Suisse Global Investment Returns, MSCI ACWI / ACWI IMI, Visual Capitalist, LPL Research

With the U.S. today accounting for nearly two-thirds of global market capitalization, the lesson is not that the U.S. will necessarily repeat Japan’s experience. Rather, it is that market leadership changes, often in ways few investors anticipate. Periods of extreme dominance, no matter how compelling the narrative, have historically proven temporary.

Investor takeaway: Concentration builds wealth; diversification preserves it. Business owners and executives with concentrated stock positions understand this instinctively. Thoughtful diversification can include not only diversifying equity holdings but adding bonds, real assets, private markets and more.

6. Assuming High Valuations Mean a Crash Is Imminent

Do High Valuations Predict a Market Crash?

Yes, valuations are elevated with the S&P 500 trading at a forward P/E of approximately 22 compared to the 25-year average of 16.7.[1]

But here’s an important insight: Valuations are poor predictors of performance over the short-term.

High valuations can stay high or move higher. Low valuations can remain depressed for extended periods. The following illustrates why valuations matter far more over longer horizons than over short ones.

Sources FactSet, dimensional.com, sparkwealthadvisors.com, ishares.com, slickcharts.com

Investor takeaway: Use valuations to set reasonable long-term expectations, not to time markets.

7. Failing to Control What You Can: Taxes

Why Tax Efficiency Compounds Over Time

Markets are unpredictable. Tax drag is not. And unlike markets, it compounds quietly and predictably.

For high-net-worth families, taxes are often the single largest “expense” on investment returns yet they’re frequently treated as an afterthought. The difference between pre-tax performance and after-tax wealth can compound meaningfully over time.

Unnecessary realized gains, poor asset location, short-term trading, and missed loss harvesting opportunities can widen the gap between what markets deliver and what investors actually keep. To be tax efficient, you need to be intentional. That includes:

These decisions may seem incremental in isolation. Over years and decades, they compound into meaningful after-tax advantages. Tax efficiency is not a year-end task. It’s an ongoing discipline woven into portfolio construction and monitoring.

Investor takeaway: It’s not what you earn — it’s what you keep. A durable strategy is built with after-tax outcomes in mind.

8. Managing Your Wealth Without an Integrated Strategy

The final (and often most costly) mistake is letting wealth drift without intentional direction. Business ventures, careers, family, health and more all compete for your attention. You make decisions incrementally, quietly add positions to portfolios, and leave assumptions unexamined. What began as a thoughtful approach can slowly turn into a set of disconnected choices.

But strong outcomes rarely happen by accident. They come from clarity of priorities, disciplined decision-making and ongoing integration across goals, spending, investments, risk, liquidity and tax strategy. Life does get busy. This is precisely why it’s essential to assemble the right team of advisors who understand your objectives, challenge your assumptions and keep your plan on course when markets or life circumstances become uncomfortable or complex.

Investor takeaway: Without a clear strategy and someone accountable for coordinating it, even smart decisions can lead you off course.

Final Thoughts: Preparing for a Range of Outcomes

Innovation, resilient earnings, and supportive policy trends often fuel markets. At the same time, elevated valuations and ongoing uncertainty remind us that risk never disappears. Progress and volatility can coexist.

The objective is not to predict what happens next. It is to prepare for a range of outcomes. Be intentional in how you deploy capital across investments, spending, philanthropy and legacy. Durability rarely happens by accident. And as always, if you or someone you care about would benefit from thoughtful guidance, please reach out to me or any of us at MKD Wealth.

Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on MKD Wealth research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss. Benchmark and index performance results do not represent any managed portfolio returns. An investor cannot invest directly in a presented index, as an investment vehicle replicating an index would be required. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from index performance shown. The following indexes are referenced in the content above:

[1] Jan. 8, 2026: Trendonify and FactSet

[2] ishares.com

[3] dimensional.com

[4] sparkwealthadvisors.com

[5] slickcharts.com

This material is for educational purposes only and is not intended to provide specific advice or recommendations for any individual and does not take into consideration your specific situation. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Be sure to consult with a qualified financial advisor, legal, and/or tax professional before implementing any strategy discussed here.

This material is for educational purposes only and is not intended to provide specific advice or recommendations for any individual and does not take into consideration your specific situation. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Be sure to consult with a qualified financial advisor, legal, and/or tax professional before implementing any strategy discussed here.

Related articles

Cybersecurity for High-Net-Worth Families and Entrepreneurs: Part 2

Cybersecurity for High-Net-Worth Families and Entrepreneurs: Part 1

Why Entrepreneurial Wealth Often Breaks Down Across Generations