With the new year underway, it is the perfect time to take a look at your financial plan and determine what proactive changes you can make in 2026 to help improve your annual financial picture and longer term outcomes.

Key Financial Planning Considerations for 2026

Here’s a breakdown of what’s changing and how proactive planning can help you stay ahead.

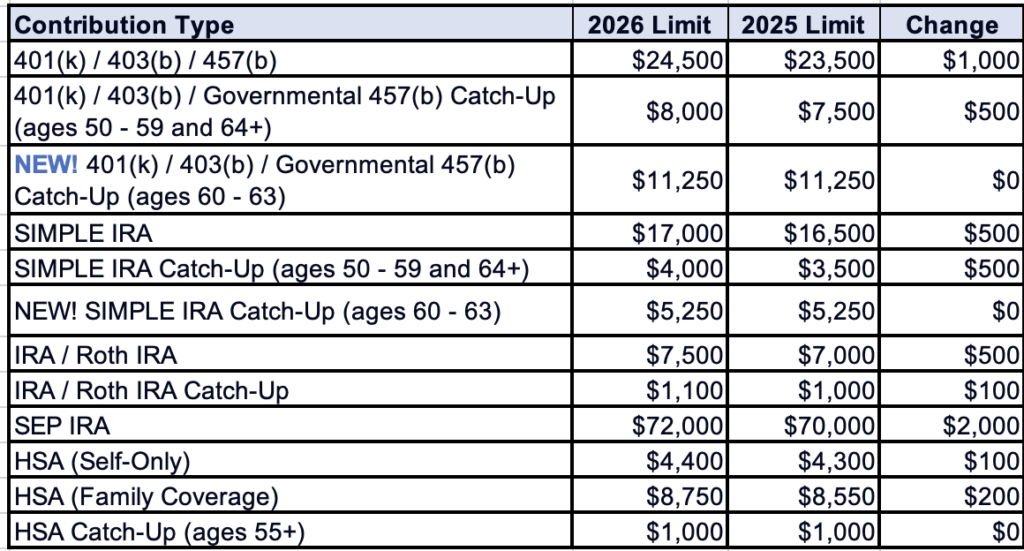

Higher 2026 Retirement Plan & Health Savings Account Contribution Limits

If you contribute to a 401(k), 403(b), or similar employer-sponsored retirement plan and expect to maximize contributions, the start of the year is a good time to review your deferral rate and catch-up elections to ensure they’re set up appropriately for 2026.

Contribution limits are updated annually, and the table below reflects the maximum contributions permitted for 2026 across common retirement and health savings plans.

Catch-up Contributions Have Specific Rules:

- Standard Catch-Up Contributions (Ages 50–59 and 64+): Individuals age 50 and older are generally eligible to make catch-up contributions in addition to the standard employee deferral limit. The standard catch-up applies for ages 50–59 and again beginning at age 64.

- Enhanced Catch-Up Contributions (Ages 60–63): Individuals ages 60–63 are eligible for higher, enhanced catch-up contribution limits. These enhanced limits are intended to support accelerated savings in the years immediately preceding retirement and may require a separate election through an employer’s plan.

- NEW! Roth Catch-Up Requirement for Higher Earners: Beginning in 2026, employees earning $150,000 or more in FICA wages (based on 2025 income) must make all catch-up contributions on a Roth basis for 401(k), 403(b), and 457(b) plans. Pre-tax catch-up contributions are no longer permitted for this group, and updated payroll elections may be required.

Because these rules vary by age, income, and plan administration, reviewing elections early helps ensure you implement contributions correctly and in alignment with your broader planning strategy.

2025 Contributions to an IRA, Roth IRA, or HSA

You can still make prior-year (2025) contributions until April 15 of 2026. Contributions must be received and deposited by that date, so please allow time for processing if you plan to fund accounts closer to the deadline.

IRS Standard Deduction Increases

The One Big Beautiful Bill Act (OBBBA) not only bumped up the 2025 standard deduction numbers from their original 2025 levels, it also increased the amounts for 2026. Here are the new 2026 standard deduction levels:

- Single filers: $16,100

- Married filing jointly: $32,200

- Head of household: $24,150

Estate Tax Exemptions Are Higher

If estate planning is part of your financial strategy, take note of these exemptions:

- Lifetime Gift Tax Exemption: $15,000,000 per person (an increase of $1,000,001 from 2025). This amount will be adjusted annually for inflation starting in 2027.

- Annual Gift Tax Exclusion: stays the same at $19,000 per recipient

If you have a taxable estate, reviewing how these changes align with your long-term goals, liquidity needs, and family priorities can help ensure your planning remains effective beyond just tax considerations.

Medicare: Are You Turning 65 Soon?

If you are turning 65 soon, you may need to sign up for Medicare. It’s generally recommended to begin the enrollment process three months before your 65th birthday by visiting Social Security Administration, calling Social Security at 800-772-1213, or visiting a local Social Security office.

If you are covered through an employer plan, including a spouse’s plan, you may be able to delay enrolling. We recommend checking with your HR department to confirm whether your current coverage coordinates with Medicare.

If you need help navigating Medicare decisions, we partner with health insurance and Medicare specialists who can guide you through the process. Let us know if you’d like an introduction.

Claiming Social Security Benefits

If you’re considering beginning Social Security benefits, be sure that you consider all of your options and the long-term income implications. Curren MKD clients can reach out to their advisors for help with this planning if you have not already reviewed it with us.

Medical Privacy When Children Turn 18

When a child or grandchild turns 18, medical privacy laws change. You may wish to contact your estate planning attorney to establish a Patient Advocate or healthcare authorization. An alternative resource to get young adult Powers of Attorney and other essential documentation in place is Mama Bear Legal Forms.

MKD Wealth is Here to Help

If you’re a current client and have questions about how these changes impact your financial plan, don’t hesitate to reach out. If you’re not yet a client but want guidance on how to proactively plan for 2026 and beyond, we’re here to help—schedule a consultation to get started.

This material is for educational and informational purposes only and is not intended to provide specific advice or recommendations for any individual. It does not take into consideration your personal circumstances, objectives, or needs. Investing involves risk, including the possible loss of principal.

The information presented, including contribution limits, income thresholds, age requirements, and other planning-related figures, is based on current laws and regulations as of the time of publication and is subject to change. While we strive for accuracy, we cannot guarantee that all information is complete, current, or error-free.

Any references to third-party resources are provided for informational purposes only and do not constitute an endorsement or recommendation. We are not affiliated with and receive no compensation from any third-party resources referenced and assume no responsibility for their content.

You should consult with a qualified financial advisor, legal professional, and/or tax professional before acting on any information discussed here.

This material is for educational purposes only and is not intended to provide specific advice or recommendations for any individual and does not take into consideration your specific situation. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Be sure to consult with a qualified financial advisor, legal, and/or tax professional before implementing any strategy discussed here.

This material is for educational purposes only and is not intended to provide specific advice or recommendations for any individual and does not take into consideration your specific situation. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Be sure to consult with a qualified financial advisor, legal, and/or tax professional before implementing any strategy discussed here.